return on equity doesn’t reflect well on its business.")

[ad_1]

If you want to identify your next multibagger, there are some important trends to look out for. One common approach is to look for companies that: Return value Capital employed increasing with growth (ROCE) amount of capital employed. This basically means that the company has a profitable endeavor that can be continuously reinvested, which is the nature of compound interest.But after a quick look at the numbers, we don’t think so. brilliant earth group (NASDAQ:BRLT) has the potential to become a multibagger in the future, but let’s take a look at why.

Return on Capital Employed (ROCE): What is it?

For those who don’t know, ROCE is a measure of a company’s annual pre-tax profit (return) on the capital employed in the business. Analysts use the following formula to calculate Brilliant Earth Group.

Return on Capital Employed = Earnings before interest and tax (EBIT) ÷ (Total assets – Current liabilities)

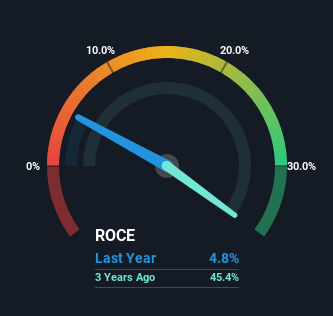

0.048 = USD 9.3 million ÷ (USD 266 million – USD 71 million) (Based on the previous 12 months to September 2023).

therefore, Brilliant Earth Group’s ROCE is 4.8%. In absolute terms, this is a low return, lower than the specialty retail industry average of 12%.

Check out our latest analysis for Brilliant Earth Group.

Above you can see how Brilliant Earth Group’s current ROCE compares to its previous return on capital, but history can only tell us so much. If you’re interested, take a look at our analyst forecasts. free A report on analyst forecasts for a company.

What can we learn from Brilliant Earth Group’s ROCE trend?

On the surface, Brilliant Earth Group’s ROCE trend does not inspire confidence. Specifically, ROCE has declined from 45% over the past three years. Meanwhile, although the business is leveraging more capital, there has been no significant change in sales over the past 12 months, which may reflect long-term investment. It could be some time before the company starts to see a change in returns from these investments.

As a side note, Brilliant Earth Group is performing well, paying down current liabilities to 27% of total assets. So we can attribute some of this to her reduced ROCE. This effectively means that suppliers and short-term creditors reduce funding for the business, reducing some of the risk factors. Since companies basically self-finance much of their business operations, we can say that this reduces the company’s ROCE generation efficiency.

The conclusion is…

To summarize, Brilliant Earth Group is reinvesting capital into the business for growth, but unfortunately it doesn’t seem like sales are picking up much yet. Investors also seem hesitant to see the trend accelerate, as the stock is down 22% in the last year. Therefore, based on the analysis conducted in this article, we do not believe that Brilliant Earth Group has the makings of a multibagger.

On another note, we discovered that 1 warning sign for Brilliant Earth Group You probably want to know.

While Brilliant Earth Group doesn’t currently have the highest profit margin, we’ve compiled a list of companies that currently have a return on equity of 25% or higher.check this out free I’ll list them here.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link